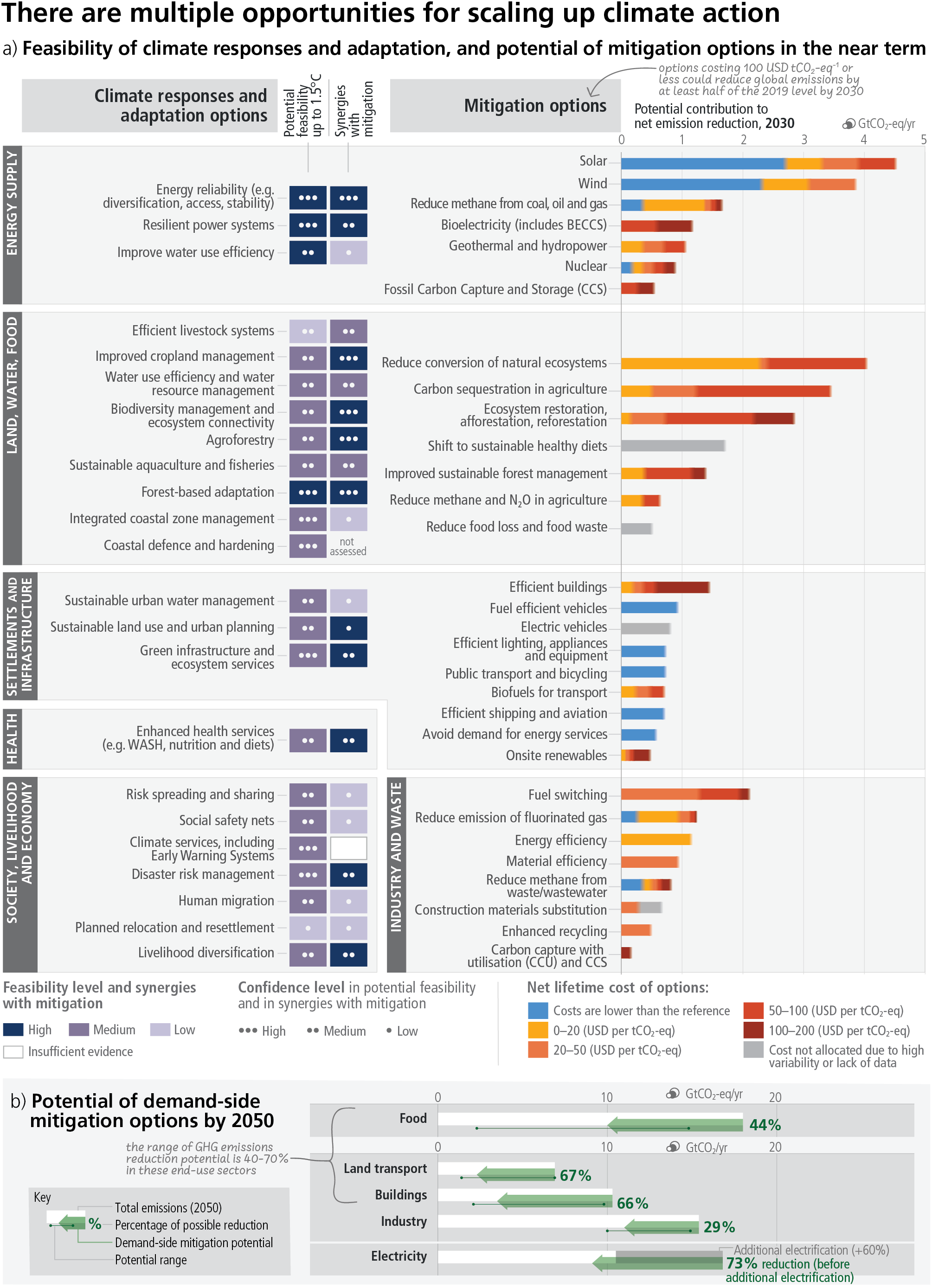

OVERVIEW

Insolvencies, production halts, and layoffs at European solar manufacturers are piling up. What's going on with European solar manufacturing? Watch a video statement (transcribed here) from our Policy Director, Dries Acke, to hear a summary of the challenges ahead and solutions to hand.

Trade Defence Measures are not part of a robust solar industrial policy

Over 420 European solar organisations warn that undertaking trade defence measures would defy the lessons of history, and be a lose-lose direction for the whole solar sector.

Read the joint statement

SolarPower Europe is working to rebuild solar manufacturing in Europe. Let's dive deeper. Why does solar manufacturing matter? Why aren't there more solar manufacturers in Europe? How do we bring solar manufacturing back to Europe? Read more to uncover the answers and discover our #MakeSolarEU campaign.

WHY DOES EUROPEAN SOLAR MANUFACTURING MATTER?

Europe is installing more solar than ever. In 2023, the EU installed over 56 GW of solar – almost three times as much as was installed in 2020.

From a total solar fleet of around 260 GW today, the EU is aiming to have 750 GW of solar capacity by 2030.

Solar is critical for Europe’s energy security and climate goals. The UN Intergovernmental Panel on Climate Change identifies solar as one of the most feasible and cost-effective methods to decarbonise the economy. From 2024, the EU needs to install at least 70 GW of solar per year to reach its climate targets.

The European Commission calls solar the ‘kingpin’ of REPowerEU – the continent’s effort to get off Russian gas. Solar panels are even featured prominently on a REPowerEU banner at the European Commission headquarters.

Given the critical role of solar in geopolitical resilience, advanced economies around the world are acting on the strategic importance of solar supply chains:

Canada

The Canadian Federal Budget of 2023 offers a 30% refundable Investment Tax Credit for investment in machinery and equipment used to manufacture clean technology - including solar.

China

Their industrial policy in the last decade has made China the world's leading manufacturer of solar components. China has invested more than US$50 billion in new PV capacity since 2011 - ten times more than Europe.

As of 2022, China supplies 80% of the world's solar PV material.

India

Since 2018, India has promoted local manufacturing of PV modules through its production-linked incentive (PLI) scheme - equalling around US$3.2 billion.

In 2023, Indian cell and module manufacturing reached 6.6 GW and 38 GW capacity respectively. Analysts predict annual manufacturing capacity will grow to 110 GW by 2026.

Turkey

Turkey the world's fourth biggest solar manufacturer, with around 8 GW of capacity in 2022. The Turkish government is aiming to join the top three manufacturers and deliver over 9 GW of solar manufacturing in 2023.

US

In August 2022, President Joe Biden announced the Inflation Reduction Act. From the SEIA, the IRA establishes two credits for solar manufacturers;

- A 30% investment tax credit (Section 48C) for eligible investment costs in facilities and equipment and

- A manufacturing production credit for certain components based on the volume of product manufactured.

USD 10 billion dollars are allocated for the Section 48C tax credits, and up to USD 6 billion dollars can support projects on land which is phasing out coal activity.

WHY AREN'T THERE MORE SOLAR MANUFACTURERS IN EUROPE?

There are two key reasons - energy costs and complex financing rules.

European solar manufacturers face energy costs two times higher than their competitors in China, and three times higher than those in the US.

Europe has retained key elements of the supply chain, like polysilicon and inverters, but energy-intensive cells, ingots, and wafers, prove challenging to reshore. Explore the interactive graph here.

Energy costs in US

20

US$ per kW

Energy costs in China

30

US$ per kW

Energy costs in EU

60

US$ per kW

Tackling the energy costs of solar manufacturing

Read the letter

While other geographies offer tax credits or direct state support, the landscape in Europe has always been trickier.

To protect fair competition between EU member states, ‘State Aid’ rules made it difficult for member states to subsidise their industries.

Industries then rely on EU-level funding - like the Innovation Fund. The Fund is being updated, but has proved lengthy and complex in the past. In the second large-scale call for funding, only 16 out of 139 projects recieved funding, and the timeline from submission deadline to receipt of grant is more than 12 months.

Enel Green Power were the only solar manufacturing beneficiary under the Innovation Fund's 2nd large scale call.

Their TANGO (iTaliAN pv Giga factOry) project, in Catania, Sicily, is set to become Europe’s largest factory producing high-performance bifacial photovoltaic modules. The total investment in the creation of the 3 GW production facility is around € 600 million, with EU funding in the amount of nearly € 118 million.

In January 2024, the TANGO plant secured a further €560 million financing from the European Investment Bank and pool of Italian banks.

HOW DO WE BRING SOLAR MANUFACTURING BACK TO EUROPE?

We fully support the Net Zero Industry Act's (NZIA) proposed target of 30 GW of solar manufacturing capacity in the EU by 2030.

We're working together with our partners at the European Solar PV Industry Alliance (ESIA) to deliver that goal.

European Solar PV Industrial Alliance

Manufacturers, developers, policymakers, and the finance community coming together to reshore European solar manufacturing.

Discover ESIAThat 30 GW goal should be achieved at each stage of the value chain, from raw material processing like polysilicon to enabling technology like inverters. It's important that the NZIA takes a full value chain approach.

The NZIA also proposes a change to the way national governments procure their renewable energy projects.

Usually a government will put to tender for a certain amount of renewable energy generation. Typically, these type of auctions are designed for the government to select the cheapest bidding project.

The NZIA would require governments to take into account other factors, not related to cost - i.e. ‘non-price criteria.’ One type of non-price criteria is sustainability, another is the geographic origin of the energy equipment.

The current proposal would makes it tougher for technologies - like most solar equipment - that are highly dependent on one supplying country to win these public tenders. We say this acts like a ‘stick’ - it discourages dependency.

However, the NZIA, and associated financing, doesn't encourage the rebuilding of European solar manufacturing. It lacks a carrot.

We propose a number of solutions to balance out the stick in the NZIA:

State Aid

EU State Aid rules were updated in March 2023 to make it easier for EU countries to support the building of solar factories, so called capital expenditure, or capex.

The rules should be further updated to support the running of solar factories - that's operational expenditure, or opex. This is particularly to help the energy intensive parts of the value chain.

Research shows that European solar manufacturing will be competitive once it reaches gigawatt-scale capacity. Updated State Aid rules would help EU solar manufacturers reach that scale.

Recovery & Resilience Facility

The RRF is an existing EU financial instrument of €723 billion which EU countries can use to support domestic manufacturing.

Part of the EU's official Guidance on how Member States can spend RRF Funds - as part of REPowerEU efforts - includes a recommendation that governments:

"need to consider providing support towards developing and expanding their industrial value chains to manufacture and recycle the low-carbon technological components and equipment needed to deliver on their energy and climate objectives. Support to industry in this respect may cover the manufacturing capacity of clean-tech equipment, notably solar, wind, heat pumps, electrolysers, and other low-carbon technologies.”

Some EU countries have already taken up this opportunity, like France, Germany, Italy, the Netherlands, Romania, and Spain.

For more case studies, check out our letter from May 2023 to national governments advising how they can use RRF funds to support their solar PV industry.

Solar Manufacturing Facility

To support a level playing field within the single market, all EU countries should have access to a dedicated EU financing tool for solar manufacturing.

We propose a the EU Solar Manufacturing Facility, a dedicated channel for EU funds to solar manufacturers. Initial calculations indicate that – in order to meaningfully jumpstart Europe’s solar PV supply chains to reach initial scale – this financial instrument would need to have access to at least €0.78 bn EUR annually to support investment of 10 GW across the solar PV supply chain over a 10-year period (totalling €7.78 bn EUR). This would cover capital expenditure and operational expenditure for partially re-shored manufacturing capacity.

The SMF would also create a venue for solar buyers and producers to sign deals. Financing could be sourced either from existing EU funding, like the Innovation Fund, or new EU funding, for example in the form of a European Sovereignty Fund, and should be supported by the European Investment Bank, with a specific role for Member States to ‘top up’ financing to draw investment to their country.

Non-Price Criteria

The ‘non-price criteria’ in the NZIA must be clear, comprehensive, harmonised, and applied only in technology specific auctions.

Right now, the NZIA proposes that technologies with a 65% dependency on one source are negatively rewarded in public auctions. However, it's not clear how we could calculate the 65%. For example, we could consider the market share relating to the final product, or an average of input materials and components going into a final product.

We're asking EU lawmakers to further detail and clarify these technical specifications within a dedicated Delegated Act.

It's also not clear how much weight that non-price criteria could have.

We recommend that sustainability and resilience criteria should count for no more than 30% of the points that can be awarded in a tender.

WHAT ABOUT INVERTERS?

Inverters Explained

Setting an EU inverter manufacturing target. Ensuring harmonised technical standards. Pairing inverters and non-firm grid connections to support the grid.

Discover the brain of the solar systemMAKESOLAREU VIDEO SERIES

Downloads

How to save the renaissance of European solar manufacturing

The SolarPower Europe board makes clear the support tools which the Industry are proposing, and that trade barriers are not the solution.

Read the statement

Read the statement

Record-low solar module prices risk EU's open strategic autonomy

Facing a perfect storm for prices in the solar supply chain (see also 'Saving European Solar Manufacturing' paper) SolarPower Europe writes to the European Commission warning of the risk of bankruptcies, and to offer solutions.

Read the letter

Saving European Solar Manufacturing

An analysis of market conditions in the first half of 2023 causing record-low solar module prices, and its implications for European solar manufacturers.

Read the analysis

The Net Zero Industry Act

SolarPower Europe's formal response to the Net Zero Industry Act's publication in March 2023.

Read the position paper

Keep the NZIA focussed

Industrial policy requires focus. The Green Deal Industrial Plan and the Net Zero Industry Act should support the most climate critical technologies, with vulnerable supply chains.

Read the joint letter

Running costs are critical

European solar manufacturers face energy prices two times higher than China and three times higher than the US. Industrial policy must reflect this.

Read the industry letter

A full value chain approach

We can only benefit from solar energy if we have the enabling technology. Inverters are the brains of the solar system.

Read the letter from inverter leaders

Using existing EU funds wisely

EU member states have access to the €723 billion Recovery and Resilience Facility, which they can use to support domestic solar manufacturing. A number of countries already are. We shared best practice with EU governments for inspiration.

Read our letter to European governments

Before the Green Deal Industrial Plan

Following the US Inflation Reduction Act publication in summer 2022, 13 solar CEOs expressed concern that Europe could fall behind in the global solar race.

Read the joint letter

Links

Discover SolarPower Europe's Manufacturing Workstream

Get to know our flagship work on supply chain sustainability

Deep dive into the brain of the solar system with our 'Inverters Explained' paper

Understand the IEAs Special Report on Solar Supply Chains

Look back at SolarPower Europe's legacy on manufacturing

FuturaSun's role in reshoring solar manufacturing to Europe

Oxford PV's role in reshoring solar manufacturing to Europe

Solarstone's role in reshoring solar manufacturing to Europe

Interested in becoming a member?

Why become a member?

Do you want to stay up-to-date about solar energy?

{kind=link}